Is It Time For Health Insurance To Go Back To The Classics?

What Happens When Market Risk Is Not Priced In

When thinking about medical needs and how to pay for them, it is natural to be concerned and have doubts about America’s health care finance system. Your health is at stake, the costs could bankrupt nearly anyone, and prices have been rising at an alarming rate for decades. Naturally, a responsible person will ask, “what if I get sick or have an accident and I’m not able to pay?”

In addition, America’s medical finance system is dominated by third-party payers: Medicare, employer sponsored health insurance, and the ACA Marketplace. Nearly no one in the State media network discusses this, but that is precisely the reason for prices rising at an alarming rate for decades. The price mechanism of free markets does not exist. And since the State likes to keep track of spending, medical care tripled to 15% of GDP in 2005 from 5% in 1960, has hovered around 18% of GDP since 2010, and GDP has soared.

To a reasonable observer, this is obscene. The price of nearly everything else has gone down or stayed in line with monetary inflation. But to an altruistic observer, this is necessary because medical care is a right and it is the State’s responsibility to take care of “those in need.” For the latter who rationalize the high costs, medical workers are sainted as “essential workers” and health insurance executives are demonized as greedy businessmen who overcharge premiums, deny claims and force you to pay high copays.

Certainly, physicians and nurses are skilled and dedicated professionals with unusually rigorous training, but it’s a vicious cycle. State regulations force them to accept the compensation and working conditions of big health corporations who must comply — and consumers to accept a limited set of medical financing options.

Medical Financing Markets

For what it’s worth, I was forced into this quagmire in October 2018. As I was no longer eligible for an employer sponsored plan and under the age of 65 in America, I was required by law to participate in the ACA Marketplace or pay the “individual mandate” tax penalty. Fortunately, the individual mandate crime was practically eliminated a few months later, but it had been enforced for eight years under Obamacare.

I chose the Gold Plan offered by Ambetter in the State of Ohio. The premium was higher than other companies but it seemed the best value based on coinsurance amounts. According to the Urban Institute, the lowest Gold Premium in Ohio for a 40 year old averaged $450 per month, but I was 62 and paid well over $700 per month. Bear in mind, premiums had increased by about 35% from the previous year due to lousy government forecasts of participation rates by healthy, young people.

The good news is that pricing had some risk parameters; the bad news is that Ambetter and I were forced to accept a comprehensive plan with overwhelming State requirements. The ugly news is that more complexity is added by individual state authorities. Each one has its own department for the regulation of insurance products. Why? It goes back to an 1869 Supreme Court ruling (Paul vs. Virginia) that stipulates insurance is not the transaction of commerce. You can’t make that up. And in 1945 an act of Congress (McCarron-Ferguson) rationalized individual state regulation to be in the “public interest.”

There may be some truth to that — it helped insulate insurance companies from federal antitrust laws. In summary, those are some causes of the pricing travesty, and the Center for Modern Health (CMH) describes their effects:

Insurers were blamed for delaying and denying patients’ care for profit. And Big healthcare corporations are now blamed for both denying care and promoting bad care for profit. Finally, the profit motive itself is blamed for the loss of patient choice and the unaffordability of healthcare. But the profit motive in healthcare, like the pricing signal, is deeply distorted.

However, it is not possible to reverse these effects without reversing their causes. And that is not possible without understanding that the situation above is a big success for the so-called health care rights activists. Why? Because everyone is blaming the insurance companies — not the government protection racket. In fact, one of their CEOs, Brian Thompson of United Health Care, was shot in the back and murdered last year by an ignorant coward in New York City and millions of douche bags on social media have joined the mob.

But why? To achieve that level of primitive behavior, President Obama’s 2014 Affordable Care Act (ACA) restricted the most important type of medical insurance: low cost catastrophic coverage for injuries and emergency illnesses with deductibles and co-pays that encourage responsible claims. Not only was the name of the Act a successful lie, but personal responsibility is also the primary target of reprogressive ideologues.

And to drive that home, the ACA also banned health insurance plans with denial of coverage for preexisting conditions. For “health care rights” to succeed, your formed habits of healthy diet, aerobic exercise, alcohol avoidance, and chemical independence must be disavowed. But that’s not all. Someone else must be held accountable for this normalization of mediocrity — annual and lifetime coverage limits were also eliminated from health insurance plans. In essence, this sacrifices a basic precept for civilized societies: rational judgment through risk assessment. Making an example of insurance companies, if we are not permitted to differentiate behavioral risks in others, that mentality reduces us to instinctual animals. That is the point.

The premise is that everyone has the same needs, complexity is the progressive trademark, and your dependence replaces their reliability. The practice is that higher income earners subsidize the costs of comprehensive coverage for middle earners and taxpayers subsidize the comprehensive coverage for lower earners — also explained by the CMH:

The only way they could sell such an unprofitable product as big health insurance was by hiding its unprofitability and resultant unaffordability through tax subsidization. Tax subsidies prevent every form of big health insurance from collapsing due to giant premiums that no one would or should pay.

In a civilized world, successful companies offer products that meet customer’s needs, are easy to use, and are reliable — yet government mandated comprehensive health coverage is none of that. In fact, third party government mandated payers drive up costs in a vicious circle of bureaucratic inefficiency that is in the same league as the public education and green energy scams.

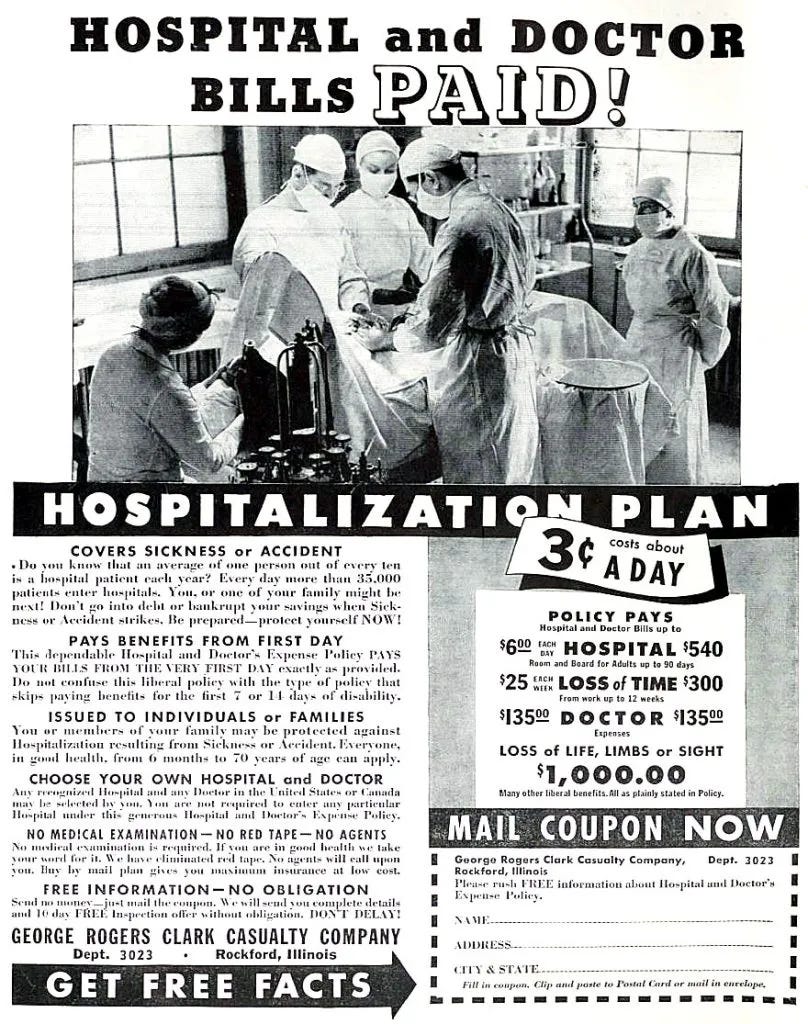

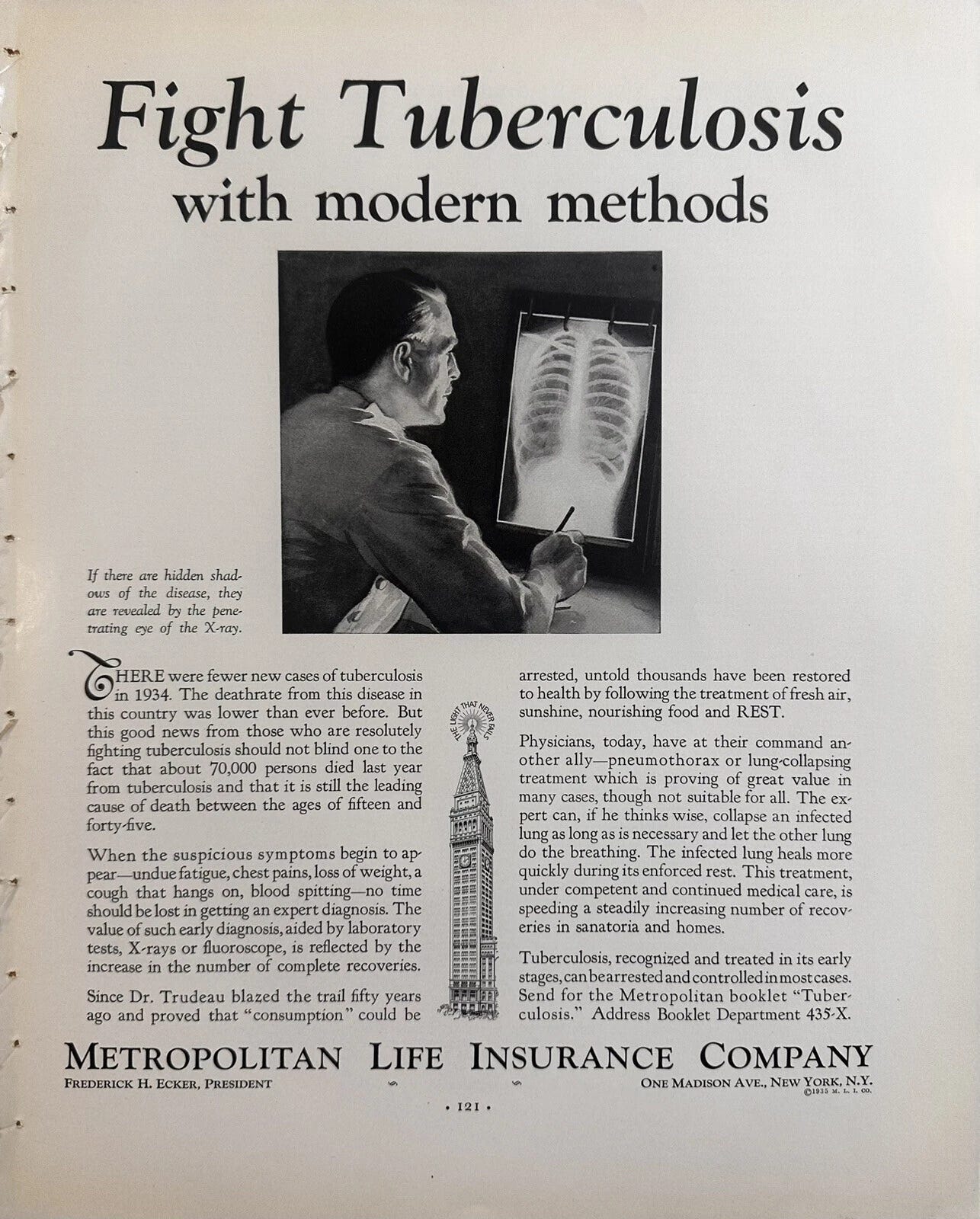

And in the 1940s and 1950s America, such a world did exist for health insurance. Notwithstanding the detrimental effects of third-party payers on the medical service pricing, individual coverage was priced according to age, health history questionnaires, preexisting condition exclusions, occupation, claims history, and geographic location.

In that environment, consumers knew what they were buying, how it was priced, and could shop for the best combination of benefits, premiums, and copays. And in group circumstances, insurance companies could avoid the adverse selection of sick people applying for insurance because the employee group existed for entirely other purposes — and they were generally younger. That is the world I remember before a neo-Marxist was elected President. The distortion began when customers with high and predictable behavioral risks were forcibly pooled with low-risk customers.

The Moneyball Method

Today, nearly everyone is limited to employer sponsored plans that cover about 54% of the American population, Medicare that covers everyone over age 65 and not covered by an employer, and the ACA Marketplace debacle. And within employer plans, you may be able to choose a Preferred Provider Association (PPA) or Health Maintenance Organization (HMO) structure — plus a Health Savings Account (HSA) with tax deductible contributions. It is their duty and no one is perfect.

Bear in mind, all insurance companies (not HSAs) are third party payers that disrupt the price mechanism for medical services. This is magnified when the price mechanism for health insurance itself is corrupted, yet no one seems to care. Someone else is paying the bill. And that is another effect of the illusion of free money caused by faith in government currency. As CMH also points out, this mentality goes back a century — to the birth of progressive nihilism:

The AMA hated the idea because they didn’t want third-party insurers inserting themselves into doctors’ clinical decisions. The insurance industry rejected the idea because comprehensive care undermines the logic of traditional insurance and would be wildly unprofitable and expensive.

In summary, this can be reinverted, but only when the culture rejects the altruistic moral code of self-sacrifice, the egalitarian excuse for acting like predetermined animals, and governing policy that is reversed to Moneyball Method principles: your sovereignty and market efficiency. For first steps in that direction, the Center for Modern Health has recommendations:

Legalize catastrophic health insurance so patients can shop for coverage that truly protects them against the financial risk of large, unexpected medical bills.

This is the best use for nearly all types of insurance. The more each person is paying for routine medical services directly, the more they will shop for the best value, determine what fits their needs and resources, and help create an efficient market. Because they only accept direct payment, the Surgery Center of Oklahoma is a premier example.

Explicitly legalize other payment models and insurance types so patients can choose alternatives to big health insurers for comprehensive healthcare services.

This is so obvious it barely needs explanation. Voluntary production and trade is fundamental to civilized societies, but both President Obama and First Lady Hillary Clinton introduced legislation that was dominated by criminal penalties.

Repeal Certificate of Need laws so that alternative payment models are free to compete against and offer alternatives to the big health insurance-based healthcare systems.

Certificate of Need laws are regulations at the state level that give bureaucrats the power to control the creation of new medical facilities, the purchase of major equipment, and expand services. This became an issue during the Covid virus panic of 2020, but to centralize control over the supply side is both immoral and impractical — because it is immoral.

Give all individuals and their families access to health savings accounts.

Health Savings Accounts (HSA) give employees of the companies that offer them a tax incentive to save money and control how it is spent. On top of that, it is a tax advantaged way to build wealth and there is no reason that everyone should not have this privilege — if it is to exist at all.

Give individuals the same tax benefits as employers to shop for their own healthcare.

Not surprisingly, employer sponsored medical insurance plans in America became popular as the unintended consequence of draconian economic policy. During World War II, strict wage and price controls were in effect and health insurance was considered a fringe benefit. Accordingly, the coverage was not treated as taxable income to employees, the costs were deductible to employers, and employers could increase the total compensation to employees without violating frozen wage laws. Today, the same benefit would mean a reduction to Adjusted Gross Income on Form 1040 equal to premiums paid.

The Aftermath

With those reforms in place, you will then be able to judge your medical financing options as an objective investor using the whole of life philosophy — and measure success by looking into the future.

Imagine large low-risk pools insuring themselves against low probability, unpredictable, but catastrophic possibilities. Traditional insurance worked precisely in this way. If, say, 100 healthy 25-year olds insured themselves for

$1000 a year each, the chances of any of them needing that money would be rare. But if even one of them needed it then they could get $100,000 from the pool in the first year itself.

Suppose one among them has a known high cost condition or adopts a dangerous habit — his health profile would be a predictable, elevated risk. The pooled money would be in heavy danger of being depleted due to his health profile. He could be asked to pay a higher premium, quit smoking or leave the pool altogether. The other 99 members of the pool wouldn’t be forced to burden themselves with his high risk profile. It is no longer a random misfortune but a pre-existing predictable risk. That is how insurance coverage became the starting point for health care financing strategy and a contingency plan for these extreme events. No matter how it functions today, that is its original actuarial basis.

Consumer choice, what a concept — and free of State tax perks and punishments.

The modern system where 99 people are forced to absorb the known high-risk problems of 1 person is an abdication of the right to freedom of association. No one should be forced to associate financially with someone who will pose a high risk to their finances. Yet, it is happening everyday and everyone in the country is paying the price for these forced associations. You wouldn’t force someone to marry a smoker. Yet it seems socially permissible to force financial pooling with one.

Unfortunately, neither major political party is serious about repealing Obamacare or any of the other laws that force prices higher for hospitals and consumers. The likelihood of these laws changing is very low. Yet, the stated Republican priority of consumer choice and tax incentives to replace entitlements and mandates is a bright spot and gives us hope for the future.

Very informative!