Why Do Rich People Give Money At High Risk To Strangers With An Idea?

To understand the nature of capitalism, we must first understand the nature of capital. And I don’t mean capital that is acquired and controlled by force, but capital that is led by free minds operating in free markets. Since capital includes productive land and mines, equipment and buildings, money and securities, knowledge and understanding, I will focus on capital in its most liquid form — that which is most easily converted to material goods and services — money and cash equivalents. And to get to the history of venture capital in its modern form, we must understand the nature and purpose of money.

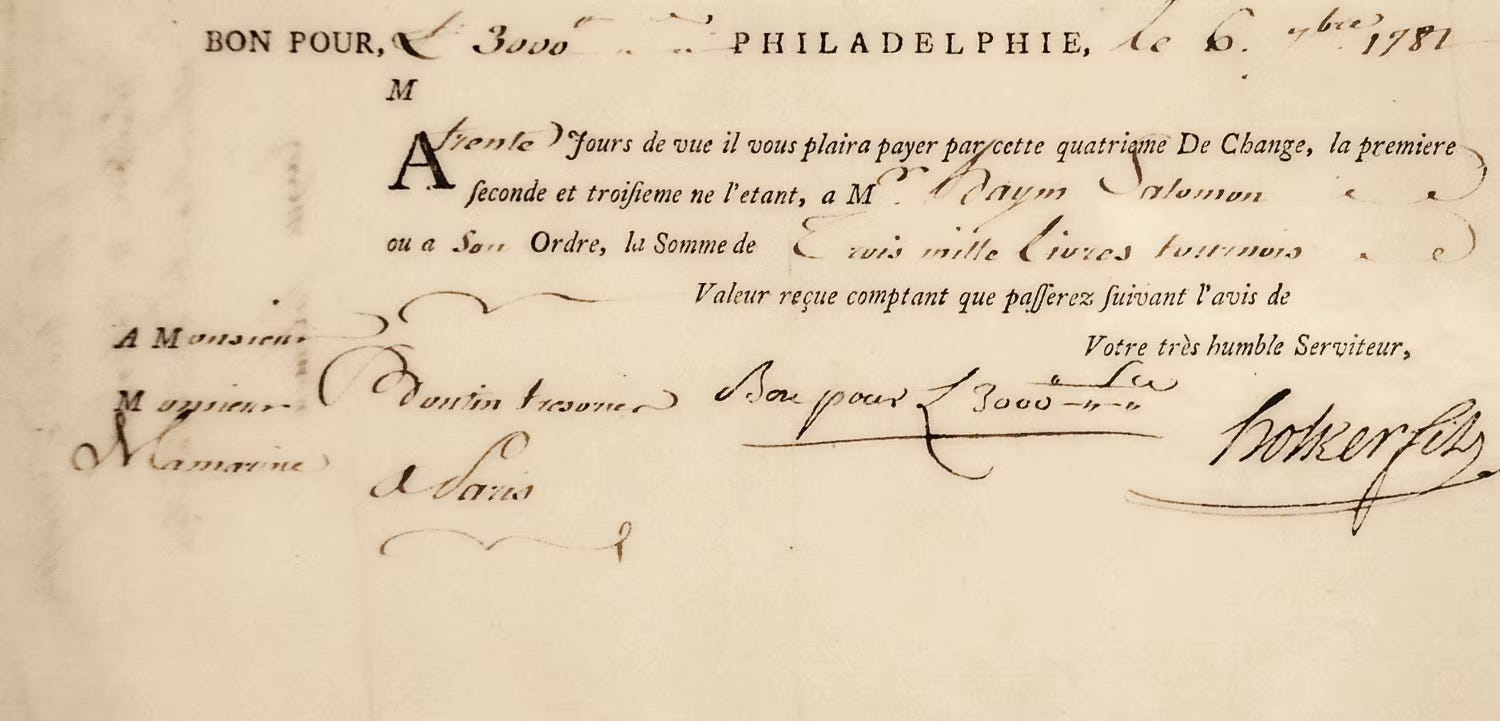

To begin at the beginning, the Lydian empire’s coinage of the Slater in the 7th century BC set the stage for the development of classical Greek civilization. And in modern times, Bills of Exchange issued by the governments of France, Spain and Holland were brokered by Haym Salomon to American merchants and bankers for the hard currency needed by General Washington to finish the war with the British at Yorktown, Virginia in 1782.

In both cases, the money had earned universal trust because it had been verified for weight and purity and was therefore easily converted into goods and services. Ultimately, money operates for the mutual profit of everyone — including people who are external to the transactions.

The Evolution of Risk Capital

Why is that important? Because risk capital — money dedicated to long-term opportunities with a high likelihood for losses — drives the discovery, invention, innovation and distribution of life-enhancing ideas from creative minds that change the future for the better. Not bank deposits, debt instruments, precious metals, or real estate, but equity. Therefore, risk capital is stock, preferred stock, stock options or any combination that gives investors the potential return that their exceedingly high-risk entails.

But more specifically, and very briefly, there are stages of development for young businesses that may attract different types of equity investors — and that depends on the distance for bringing product to market and the distance for cash flow to profitability.

Initially, founders and inventors will finance their own product development in a stage known as bootstrapping that may be supplemented with capital from friends and family. The next layer are angel investors who have confidence in the principals, the efficacy of their ideas, the risk capacity to lose, and a low time preference.

At the next layer are the professional investors who deploy pooled risk capital. These are venture capital (VC) firms who take stakes in younger companies and private equity (PE) firms that invest in more profitable enterprises. In both cases, they have aggressive growth targets, take minority (VC) or majority (PE) control, and have relatively short time horizons for a liquidity event (4-7 years).

A liquidity event is typically the sale of the company to another corporation or the sale of the company to public shareholders through an initial public offering (IPO). In turn, the IPO transaction is managed by an investment bank that markets and distributes the shares to institutional and retail investors, after which the stock trades on a stock exchange like the NYSE or the NASDAQ.

Nearly all investors, including those who employ The Moneyball Method, buy and sell shares of stock in companies on these secondary markets, but that is not what this article is about. In part, this is about the irrelevance of governing authorities for creating wealth and prosperity for mass populations. Whether it is Sumerian kings and their power over grain producers or the Federal Reserve and their access to technology producers, they produce nothing.

Because money is created by producers, its supply is actually governed by them. And money is not stupid, as journalist John Tamny, author The Money Confusion observes,

“That Friedman was so wise, and Bernanke was at least book smart, causes one to wonder. How could they have fallen for such an absurd viewpoint as the Fed playing the insurmountable barrier to credit inflows? Money always finds opportunity, without regard to international borders. Attempts by central banks to render credit expensive or cheap . . . are toothless relative to existing incentives for the resource-rich to match their capital with talent.”

And so, I decided to write this tribute to risk takers. To profess my gratitude for the effects of stable, anonymous money invested by the “resource rich” who appeared on the scene — for the first time in history, with the industrial revolution spawned by the Age of Reason.

America’s Gold Standard

Naturally, liberty creates incentives — and with slavery banned in England, and then America, it is poetic justice that America’s return to the gold standard after the Civil War coincided with Thomas Edison’s application for a patent on his electric lamp. The year was 1879 - and the flow of capital and the flow of electrons became two sides of the same coin.

In fact, Edison addressed public lighting as an integrated system of generating stations, distribution networks and powerful investors. But it began with his bootstrapped Quadruplex telegraph system that he sold for $30,000 in an 1874 liquidity event to fund his Menlo Park laboratory.

Ten years after Edison’s patent application and JP Morgan lighting his personal home and office to demonstrate, Morgan advised Edison on the merger of his different business units into Edison General Electric Company. The year was 1889, but three years later Edison was out as a director of the combined enterprise after it’s 1892 merger with Thompson-Houston Electric. The new company was called General Electric, and control was allocated to Thompson’s president with their AC patents and industrial research lab.

Which brings us to George Westinghouse and the formation of Westinghouse Electric in 1886. The man was a serial entrepreneur who bootstrapped the invention of his railway air brake system, solicited angel investors to create Westinghouse Air Brake Company in 1869, and reinvested his fortune into the gas distribution business. With that experience, he believed there were more efficient ways to distribute electricity, and formed Westinghouse Electric in 1886 by reinvesting again — private equity.

Two years later he bought the alternating current (AC) patents of Nikola Tesla for $1 million, hired Tesla away from Edison, and eventually won the contract to illuminate the 1893 Columbian Exposition in Chicago. Also known as the current wars, AC and the transformers patented by Tesla in 1890 became crucial for power grid development.

And no discussion about hands-on venture capital in America would be complete without referencing J. P. Morgan’s contributions to power distribution, railroad capitalization, and steel production. By 1900, Morgan controlled over 100,000 miles of track, but many lines were failing and saddled with debt. With the help of other Wall Street bankers, unprofitable lines were consolidated and debt was cut by one-third. Ultimately, the minds of Morgan and banking partner Anthony Drexel could see the value hidden beneath inefficient financial statements — and they were able to streamline the operation of the American railroads and steel manufacturing businesses they controlled.

However, Morgan’s greatest strategic move was his buyout of Andrew Carnegie in 1901. Carnegie named his price, a grossly inflated $500 million, and Morgan accepted without hesitation. He then consolidated that with several smaller steel firms to create US Steel — a feat that is unimaginable for government bureaucrats — and therefore intolerable to them.

The Technology Revolution

It is all too common for statists who only destroy wealth to condemn bankers for being parasites — a label that belongs exclusively with these critics. In fact, it was the communists, socialists and progressives who in condemning money and banking — gave us antitrust regulations, World War I, World War II, the welfare state and the monetary devaluation that made all of that possible.

However, reality always wins, venture capital envisions our future, and in 1946, the American Research and Development Corporation (ARD) was hatched. It was the first American firm to choose companies on behalf of investors - rather than drawing from family wealth. Led by a French immigrant president, Georges Doriot, ARD declared a new approach to entrepreneurial finance:

“ARD does not invest in the ordinary sense. Rather, it creates by taking calculated risks in selected companies in whose growth it believes.”

Also believing in this philosophy were the individuals who comprised 43% of ARD’s original capital, 36% from investment companies, 8% from insurance companies, 7% from brokerage firms, and 6% from higher education. Initially, very few of its portfolio investments were successful, and as a closed-ended mutual fund listed on the NYSE, ARD’s share price fell 29% to $16 by 1954.

But in 1957, everything changed. ARD bought a controlling interest in Digital Equipment Corporation (DEC); a company that had developed circuit board modules and would eventually produce high speed computers at a fraction of the cost of rival IBM:

The DEC investment showed that a VC firm could build a portfolio of long-tailed investments; the return of the few that hit the long tail would offset the losses and mediocre gains of the others.

ARD supplied both capital and governance. It was not only selective about the initial investments it chose to make, but it actively participated in the management of those companies.

By creating opportunities for wealth accumulation, ARD created an entrepreneurial demand-side spur to venture capital.

The firm's prized portfolio companies also included Circo Products (automobile tools); High Voltage Engineering Corp (high-powered generators and nuclear particle accelerators); Tracerlab, Inc. (analytical instruments and radiation detectors); Baird Associates (chemical analysis instruments); and Ionics (water purification). Doriot did not believe in turning companies around for an instant profit but rather staying with them for the long term and through challenging periods.

The Enlightenment spawned the American Revolution and the banning of slavery spawned the Industrial Age, but it was reliable money anchored by gold that played an essential role in these developments. And the story just keeps getting better.

Before the creation of American Research and Development Corporation in 1946 and the success of Digital Equipment Corporation after 1957, there was no individual investor demand for VC opportunities. Government spending had crowded it out. But now that there was venture capital with skin in the game, and soon there would be the biggest game changing development — Silicon Valley.

The signature event took place in 1968 at the Fall Joint Computer Conference hosted by the Institute of Electrical and Electronics Engineers. There, Douglas Engelbart took the stage and presented the developments of the Stanford Research Institute. His 90-minute discussion featured a complete computer hardware and software system called the oN-Line System.

For the first time, the fundamental elements of modern personal computing were demonstrated: windows, hypertext, graphics, navigation and command input, and video conferencing. It also included the computer mouse, word processing, and a real-time editor.

Known as the Mother of All Demos, Engelbart’s performance influenced the operating systems of the Apple Macintosh, the Atari ST, the Commodore Amiga, and the Microsoft Windows graphical user interface. Everything that Silicon Valley is today can be traced back to the development of venture capital post World War II and especially to ARD and Doriot.

These inventions were brought to market in the 1980s and 1990s — a time when the dollar was being removed from the gold standard and devalued across the world. But capital invested by those with skin in the game is the legacy of stable money backed by gold. The very nature of capital is that it is led by free minds operating in free markets.

There is good reason for the US dollar being the world’s preferred currency: America remains the most productive society and capital finds talent wherever it may be. For now, this is the best version of a stable society and economy that we can build, given that going back to the gold standard seems a distant mirage. But we must remember, that to maintain a civilized culture, stable money and the property rights of private individuals must become precious resources that earn morally protected status.

“We are a movement, not just a company. A commercial bank lends only on the strength of past successes and proven assets. I want money to do things that have never been done before.”

Georges F. Doriot, in the Shawmut News Bulletin, 1961